Tax deductions for Home Office expenses when working from home can be claimed if your home is a place of business, or if it is used for income earning activities.

This requires evidence of a more-than-incidental use of an otherwise private area of the house.

If your home is not a place of business, but you spend time working from or at home, then your claims are for running expenses.

This may include a portion of your electricity, gas, internet, telephone expenses and depreciation and repairs of equipment.

Electric vehicle home charging rate (2022-23 & 2023-24)

The Tax Office has published acceptable methods for the claim and calculation of electricity costs when an employee charges an electric vehicle at home.

Claim Methods For 2022-23

For 2022-23 you still have a choice of claiming the actual costs, with records of expenditure being required.

Alternatively the fixed rate method covers most running costs but allows depreciation to be claimed in addition.

The hourly fixed rate for 2022-23 is 67 cents per working hour, and this covers internet, phone, electricity, gas, stationery and computer consumables.

You can claim separately for depreciation, and it is no longer a requirement to have a home office specifically set aside for work.

Some records (e.g. of hours worked) are still required.

Hourly rate method of estimating home office deduction

Revised Fixed Rate Method From 1 July 2022

From 1 July 2022 a new guideline provides for a revised fixed rate method with a deduction rate of 67 cents per hour, which can be used as an estimate of fair and reasonable additional expenses incurred working from home.

There must be available evidence to show that additional expenses were in fact incurred.

If you have used the fixed rate method previously, you will need to be aware of the differences.

The main differences are set out in the table below.

Comparison Of This Year’s And Last Year’s Fixed Rate Claim Methods

This is a crude summary, and a guide only. Check detailed requirements before making any claim. See PCG 2023/1

| 2022-23 | 2021-22 | |

|---|---|---|

| Feature | 67 cents claim method | 52 cents claim method |

| Expenses covered by the fixed rate | ‘Additional running expenses’: Internet, phone, electricity, gas, stationery, computer consumables, repairs & maintenance of depreciable assets | Electricity and gas (for heating, lighting, and cooling), depreciation, and repairs of office furniture |

| Depreciation allowance deductions | Claimable in addition | Included in the fixed rate |

| Mobile phone and internet costs as well as computer consumables and stationery | Included in the fixed rate | Claimable in addition |

| Requirement for dedicated home office space | No | Yes |

| Period of applicability | From 1 July 2022 | until 30 June 2022 |

| Hourly fixed rate | 67 cents per hour | 52 cents per hour |

| Record keeping – hours | Record of representative hours up to 28 Feb 2023, thereafter actual hours (PCG 2023/1) | Records which establish pattern of work-related usage |

| Record keeping – other | Documentary evidence (see PCG 2023/1) | Documentary evidence and estimates where permissable |

| Alternative claim method | Actual expenses (with substantiation) | Actual expenses (with substantiation) or ‘the ‘shortcut’ 80 cents per hour method |

Draft Practical Compliance Guideline PCG 2022/D4 which sets out the basis of a revised fixed rate method to apply from 1 July 2022 has been replaced by Practical Compliance Guideline PCG 2023/1.

The fixed rate from 1 July 2022 covers the total of ‘additional running expenses’ which includes:

- electricity or gas for lighting, heating, cooling and electronic items used while working from home;

- internet expenses

- mobile and home telephone expenses

- stationery and computer consumables

- the repairs and maintenance to depreciating assets.

Under the revised fixed rate method from 1 July 2022, depreciation allowance deductions (such as for office furniture and technology) can be claimed in addition to the 67 cents per hour spent working from home.

This does not require a separate home office or dedicated work area set aside in the home.

Note that Taxation Ruling TR 93/30 “Income tax: deductions for home office expenses” continues to apply and should be considered in conjunction with the new ruling.

Fixed Rate Method Record Keeping 2022-23 and 2023-24 onwards

Additional Running Expenses

The claim is to be based on factual circumstances which give rise to ‘additional running expenses’ due to working from home.

Evidence of additional costs must be available.

For example, a taxpayer living rent-free with his parents, and making no contribution to household bills is not incurring additional expenses, and thus not entitled to claim the fixed rate method. (see PCG 2023/1 example 6).

On the other hand, a plumber who completes work at home on a regular basis in connection with his business, such as invoicing, has additional expenses, evidence of bills paid and on that basis can claim using the fixed rate method. (PCG 2023/1 example 5).

Hours Spent Working From Home

PCG 2023/1 requires that records of hours spent working from home be kept.

- For 2022-23 until 28 February 2023 the record must be representative of the total number of hours worked

- For 2022-23 from 1 March 2023 to 30 June 2023 an estimate of hours cannot be used. The record must be of the total number of actual hours worked from home

- and likewise, from 2023-24 and onwards the total number of actual hours worked from home must be recorded

See also ATO: Working from home deduction changes for 2022–23

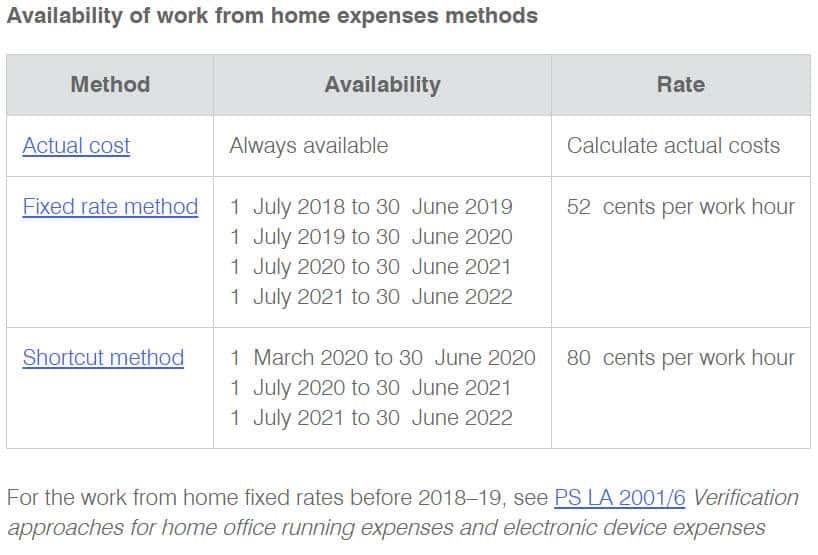

Shortcut method 80 cents per hour for all costs, from 1 March 2020 to 30 June 2022.

Claims for periods from 1 March 2020 can be calculated at the rate of 80 cents per hour.

This method can be used for tax periods

- 1 March 2020 to 30 June 2020; and

- years ending 30 June 2021 and 2022.

The optional 80 cents rate method covers all costs associated with working from home, including heating and cooling, electricity, mobile phone, internet and depreciation of office equipment etc.

The 80 cents method precludes any other home office costs being added to the claim.

By contrast the 52 cents per hour claim method only covers electricity, gas and depreciation, allowing other costs to be separately identified (see below).

Under the 80 cents method the only records required to be kept are time records, showing the hours worked from home, and there is no requirement for a dedicated work area.

Previous Years’ Fixed Rates Methods

The fixed rate method allows a claim of 52 cents per hour in the tax years 2018-19, 2019-20, 2020-21 and 2021-22.

If applicable, mobile phone and internet costs as well as computer consumables and stationery can be separately added to the claim.

Hourly rates for the fixed rate method are revised periodically. The rate of 52 cents per hour applies in the periods from 1 July 2018 to 30 June 2022.

Hourly rates:

- Years from 1 July 2018 to 30 June 2022 – the rate is 52 cents per hour

- Years from 1 July 2014 to 30 June 2018 – the rate is 45 cents per hour

- Years from 1 July 2010 to 30 June 2014 – the rate is 34 cents per hour

- Years from 1 July 2004 to 30 June 2010 – the rate is 26 cents per hour

- Years from 1 July 2001 to 30 June 2004 – the rate is 20 cents per hour

Claims For Phone and Internet

Note: these claims will only be available if not already covered by a claim method. From 2022-23, the fixed rate claim method includes phone and internet costs, so a separate claim is not allowed.

Phone and internet expenses

Mobile and home phone and internet expenses can be claimed provided there is sufficient evidence to support the requirement for the work-related usage and a reasonable basis of apportionment is used for calculating the work-related use.

Apportioned business internet usage can be estimated based on records of actual usage maintained for the year or in stable usage circumstances a representative 4 week period will suffice.

Calculations are expected to take into account such factors as bundled services, personal usage, periods of annual leave and use by other persons. Calculation examples are provided in PS LA 2001/6.

Claiming for telephone up to $50

For incidental work use of a taxpayer’s telephone where the claim is not more than $50, the ATO accepts claims based on the the following estimates:

- work calls from a landline: 25 cents per call

- work calls from a mobile: 75 cents per call

- work-related text messages sent from a mobile: 10 cents per text

Claiming more than $50

To establish a claim of more than $50, a 4-week representative period of expenditure can be used to establish a percentage claim of the total cost of calls and data contained in itemised billing records. Records include diary entries, electronic records, and bills, along with some evidence from the employer that work from home or work-related calls are expected.

Records and proof of claims

There is an overall requirement that the basis of claims calculations be “reasonable”.

For substantiating a claim,

- keep records which support the actual costs incurred, and which indicate the correct non-deductible apportionment

- keep a representative four-week diary to establish a pattern of usage. If there is no regular pattern, then records of the duration and purpose of each occasion would need to be kept.

A claim is not allowed where there is no additional cost incurred (such as a working area shared by normal domestic activity) or if the income producing activities are merely incidental.

Place of business

The Tax Office provides guidance for determining whether a home, or an area within it, is being used as a place of business. Factors to consider include whether:

- the area is clearly identifiable as a place of business;

- the area is not readily suitable or adaptable for use for private or domestic purposes in association with the home generally;

- the area is used exclusively or almost exclusively for carrying on a business; or

- the area is used regularly for visits of clients or customers.

(Source: TR 93/30)

If you are working from your home used as a -place of business, (normally this would exclude you simply acting as an employee), then further deductions for the relevant proportion of attributable occupancy expenses such as rent, interest, rates and insurance may be also claimable

But in that case the capital gains residence exemption (for home owners) may also be reduced by the proportion of work-related use. Employees are generally not able to claim occupancy costs.

More information:

- Working From Home Expenses – ATO

- Practical Compliance Guideline PCG 2023/1 Claiming a deduction for additional running expenses incurred while working from home – ATO compliance approach

- Practical Compliance Guideline PCG 2020/3: Claiming deductions for additional running expenses incurred whilst working from home due to COVID-19

- Article: Proving deductions for home office expenses, mobile phones and internet

- PS LA 2001/6 Home office and electronic device expenses (contains calculation methods and examples)

- Claiming mobile phone, internet and home phone expenses

- Tax return item D5 – Other work-related expenses 2023

- Tax return item D5 – Other work-related expenses 2022

- Tax return item D5 – Other work-related expenses 2021

- Tax return item D5 – Other work-related expenses 2020

- Tax return item D5 – Other work-related expenses 2019

- Tax return item D5 – Other work-related expenses 2018

- Tax return item D5 – Other work-related expenses 2017

- Tax return item D5 – Other work-related expenses 2016

- TR 93/30 Income tax: deductions for home office expenses

- Home office expenses calculator

- Claiming a tax deduction for expenses for a home-based business

This page was last modified 2024-02-02