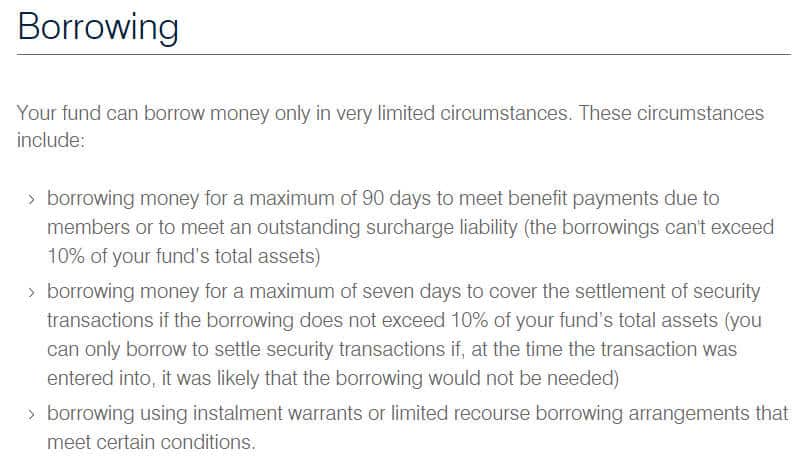

SMSF Borrowing

Super Funds with very limited exceptions are restricted in their borrowing capacity by legislation.

The ATO’s information around super funds borrowing rules in general are outlined here (click to go there):

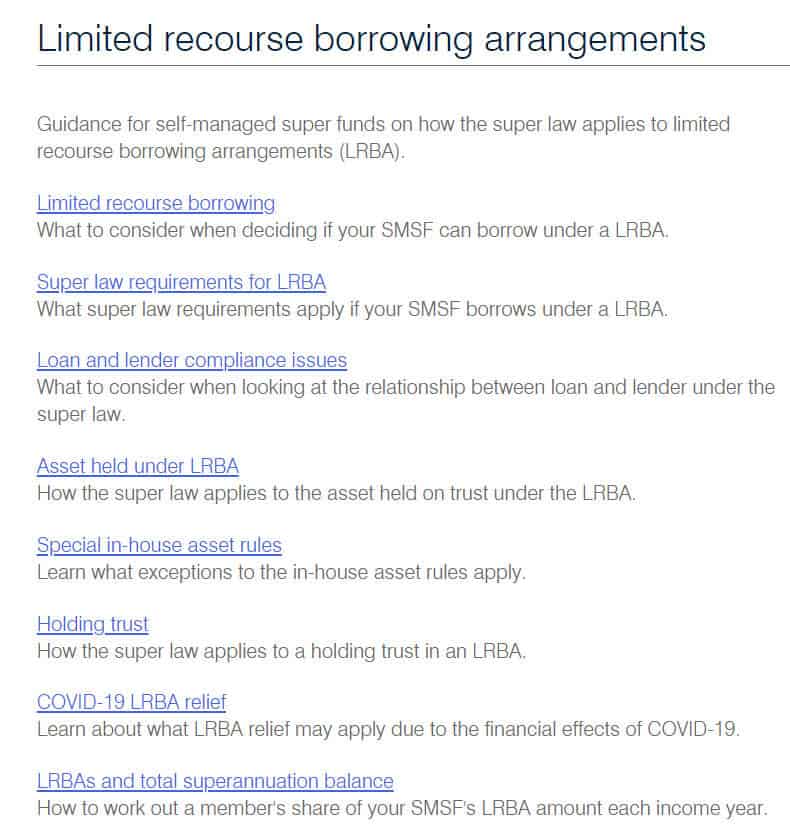

Questions and Answers regarding Limited Recourse Borrowing Arrangements and the safe harbour rules in guidance document PCG 2016/5 are outlined here (click to go there):

LRBA Safe Harbour Variable Interest Rates

| Real Property | Shares and Units | |

| 2023-24 | 8.85% | 10.85% |

| 2022-23 | 5.35% | 7.35% |

| 2021-22 | 5.10% | 7.10% |

| 2020-21 | 5.10% | 7.10% |

| 2019-20 | 5.94% | 7.94% |

| 2018-19 | 5.80% | 7.80% |

| 2017-18 | 5.80% | 7.80% |

| 2016-17 | 5.65% | 7.65% |

| 2015-16 | 5.75% | 7.75% |

For fixed interest rates trustees may choose to fix the rate at the commencement of the arrangement for a specified period, up to a maximum of 5 years (real property) or 3 years for (shares and units).

See also:

- Practical Compliance Guidelines PCG 2016/5 Income tax – arm’s length terms for Limited Recourse Borrowing Arrangements established by self-managed superannuation funds

- Super Fund Laws in Australia

This page was last modified 2023-06-30