Since 2017 and currently a non-refundable Low Income Superannuation Tax Offset is available to superannuation funds, to reduce the tax paid on the concessional contributions of low income earners.

“Low income” refers to an adjusted taxable income of $37,000 or less.

Up to $500 rebate is available, calculated as 15% of eligible contributions. Calculated amounts of less that $10 are rounded up to $10.

The LISTO is a rebate is paid to the super fund account of the low income member. The rate of 15% of eligible contributions matches and therefore effectively cancels the 15% income tax on contributions, up to the ceiling of $500.

The offset is available from 2017-18 and later years.

The offset operates in a similar manner to the earlier “LISC” scheme which was available from 1 July 2012 to 30 June 2017.

The rebate is paid to the super fund of the low-income taxpayer claimant.

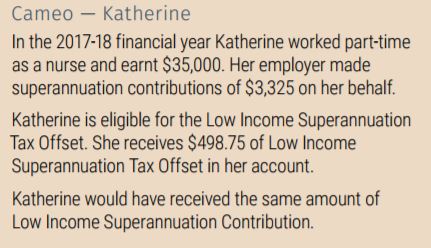

Example:

Source: ATO

Legislation was passed (in Nov 2016) by parliament to provide a rebate of up to $500 (credited to their super fund) for low income earners with an adjusted taxable income of $37,000 or less.

The rebate applies from 1 July 2017.

The amount of the rebate is calculated as 15% of eligible super contributions, which are essentially contributions made to an approved (i.e. “eligible”) super fund.

The necessary conditions are:

- at least one concessional contribution has been made by or for that individual in the corresponding financial year; and

- adjusted taxable income for that income year that does not exceed $37,000

- at least 10% of the individual’s income for the income year is from business or employment (or where in limited circumstances the Commissioner estimates that to be the case)

- the individual’s Total Superannuation Balance must be below the Transfer Balance Cap (currently $1.7 million).

- temporary visa holders (except NZ citizens) are excluded

Unlike the co-contribution requirements, there is no age limit on eligibility.

See further

This page was last modified 2022-07-15