The Dependant Spouse Offset has been phased out.

Budget Announcement 13 May 2014

The Federal Budget 2014-15 presented to parliament on 13 May 2014 contains a proposal to remove the dependent spouse tax offset for all taxpayers with effect from 1 July 2014. Enabling legislation has been passed – see Tax and Superannuation Laws Amendment (2015 Measures No. 1) Bill 2015.

Taxpayers who (under previous phase-out arrangements) were able to claim the dependent spouse offset (see below) and other dependent tax offsets under the calculations for zone and overseas forces tax offsets are also no longer be able to claim from 1 July 2014.

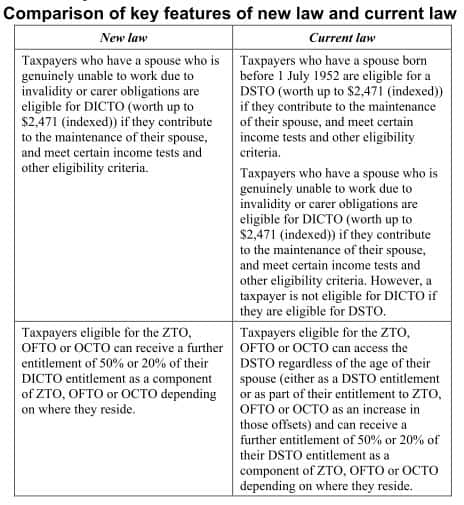

DICTO continues: Taxpayers with a dependant who is genuinely unable to work due to a carer obligation or a disability will continue to be able to claim the Dependent (Invalid and Carer) Tax Offset which was introduced to replace the range of dependents offsets more generally from 2012-13.

Age-based restrictions since 1 July 2011

From 1 July 2011 the dependent spouse tax offset is only available for a spouse

- born before 1 July 1971; or

- unable to work due to invalidity or carer obligations.

.. and further from 1 July 2012

From 1 July 2012 the offset has been further restricted to dependent spouses born before 1 July 1952

Income test

Family Tax Benefit Part B exclusion: The offset is excluded for taxpayers whose adjusted taxable income (see below) is more than $150,000, or a member of a Family Tax Benefit Part B family.

Value of offset (indexed annually)

For those still eligible to claim, the maximum dependent spouse tax offset value is:

- $2,471 in 2013-14

- $2,423 in 2012-13

- $2,355 in 2011-12

Dependent spouse’s income test

The value of the offset is reduced by $1 for every $4 by which the adjusted taxable income (see below) of the dependent spouse exceeds $282. This removes the offset value at the upper limit of adjusted taxable income of:

- $10,166 (2013-14)

- $9,974 (2012-13)

- $9,702 (2011-12)

Not Refundable: The offset can be used to reduce tax payable, but is not refundable, nor is it available to offset the medicare levy.

Residence: In general, both the taxpayer and dependant must be resident for tax purposes, and part-year claims are possible on that basis.

Adjusted Taxable Income formula

“Adjusted Taxable Income” for the purposes of claims means the total of:

+ adjusted fringe benefits (see reportable fringe benefits )

+ tax-free pensions or benefits

+ target foreign income (income from overseas not reported in your tax return)

+ reportable superannuation contributions

+ net investment lossesless deductible child maintenance expenditures.

Dependent (Invalid and Carer) Tax Offset (“DICTO”)

Taxpayers with a dependant who is genuinely unable to work due to a carer obligation or a disability are generally eligible for the DICTO which continues to be available. See details of the Invalid and Carer Tax Offset here.

This page was last modified 2018-12-10